How we are buying

Subto (Subject-To)

Subto (Subject-To)

Subto (Subject-To)

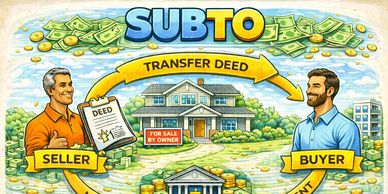

A Subject-To (or "Subto") purchase is when you buy a property and take ownership of it while leaving the seller's existing mortgage in their name — you simply take over making the payments. Think of it like taking over someone's car payments while the loan stays in their name. The big win for investors is that you skip bank qualifying and keep the seller's existing interest rate, which could be much lower than today's rates.

Seller Finance

Subto (Subject-To)

Subto (Subject-To)

Seller financing is when the person selling the property acts as the bank — instead of you going to a traditional lender, the seller agrees to let you pay them directly in monthly installments over time. You agree on a purchase price, interest rate, and repayment terms, sign a promissory note, and make your payments straight to the seller each month until the property is paid off.

Sub-Tail

Subto (Subject-To)

Morby Method

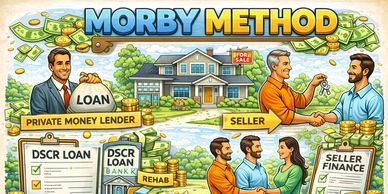

A Sub-Tail combines Subject-To and Seller Finance in one deal — you take over the seller's existing mortgage and the seller finances their remaining equity to you in monthly payments. So instead of coming up with cash for the equity gap, you simply make two payments: one to the original bank and one to the seller.

Morby Method

Private Money Partner (PMP)

Morby Method

Usually in conjunction with a DSCR loan or Private Money Lender. The loan pays the seller a portion of the asking price and the seller finances back a portion of the loan to the buyer to help with down payment, closings and possible acquisition fees and rehab.

DSCR

Private Money Partner (PMP)

Private Money Partner (PMP)

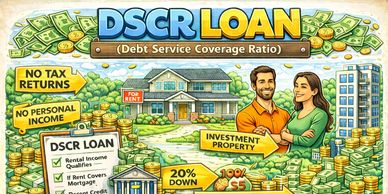

A DSCR loan (Debt Service Coverage Ratio) is a type of investment property loan where the bank qualifies you based on the property's rental income rather than your personal income or tax returns. If the rent the property generates covers the mortgage payment — typically at a 1.0 to 1.25 ratio and you have decent credit— you get approved.

Private Money Partner (PMP)

Private Money Partner (PMP)

Private Money Partner (PMP)

A private money partner is simply a regular person — a friend, family member, colleague, or fellow investor — who loans you their own personal cash to fund a real estate deal in exchange for a return on their money. Instead of going to a bank, you borrow from someone you know (or network with) and pay them an agreed-upon interest rate, typically 8–12%. They earn better returns than leaving money in a savings account .